Did you know that almost half of Americans don’t have any emergency savings?1 In the world we live in today, that’s crazy. If that’s you, you my friend are playing with fire.

Today, I’m going to share how to create a personal budget for your money that’s fun and will free up cash so that you can build what I call, your 3 Money Buckets: Your Emergency Fund, Vacation/Travel fund, and your 5-Year Goals fund.

Ah, budgets. The “B” word.

Unfortunately, budgets get a bad rap. I think it has a bit to do with people viewing budgets as restrictive, that they limit your freedom to spend and have fun. At least that’s what I used to believe. But, that’s also a time when I used to live paycheck to paycheck.

At the time, I had this misconception that financial success had everything to do with how much money you made. Today, I know a lot better. As a financial advisor, I get to witness firsthand, what works for my most successful clients, and what doesn’t work for my least successful ones.

Financial success, it seems, has less to do with how much you make, and more to do with how much you can save. It’s all about your cash flow, which is the flow of money in and out of your household.

Why is budgeting so hard?

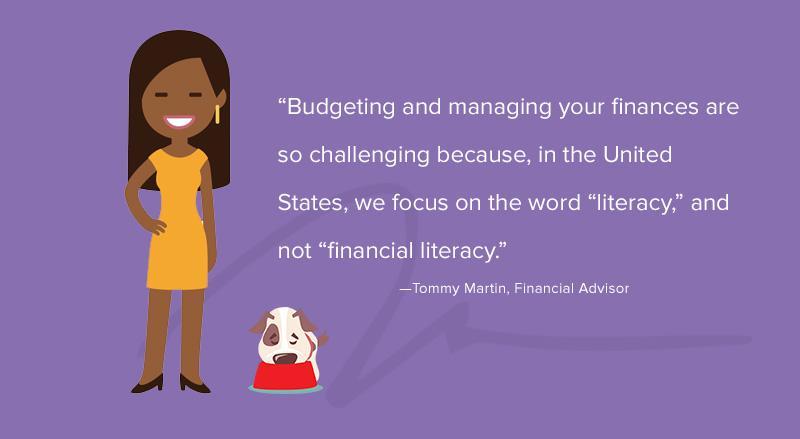

A person can be highly educated, professionally successful, and still be financially illiterate.

Roberty Kiyosaki

Budgeting and managing your finances are so challenging because, in the United States, we focus on the word “literacy,” and not “financial literacy.”2 Because of that young Americans graduate from school without basic financial skills, like understanding cash flow and budgeting or what makes something an asset or a liability.

I’m sure if people better understood how money worked, they’d be buying assets, things that make them money, over taking out car loans, furniture loans, second mortgages, and racking up credit card bills. Those purchases, when you use debt to pay for them, erode a portion of your earning potential in monthly payments.

If you want to build wealth for yourself, you need to understand numbers. Because, like words, numbers also tell a story. The question is, what story are your numbers telling?

What is a zero-based budget?

I’ve tried a lot of budgeting styles over the years and none of them worked, long-term. They ended up being restrictive and time-consuming to manage.

What finally worked for me was a zero-based budget. A zero-based budget gives every dollar that you earn a job, so it’s not restrictive. If you want your, “vanilla coconut milk cappuccino with no foam and whipped cream,” you just need to budget for it, and only if you get it routinely. If it’s just a once in a while thing, no sweat. Having a cash cushion sinking fund will cover your miscellaneous spending so that you don’t have to feel bad. For someone like me, that’s permission to spend and a win-win.

I’ll cover sinking funds later in this video. If you want to learn more about the zero-based budget, I have another video for that.

But for now, let’s cover the 5 steps to create a personal budget for your money.

5 Steps to Create A Personal Budget For Your Money

Step 1: Add up your income

This is your total take-home pay (after tax) for both you and your partner. You don’t have to be married or in a traditional relationship to do this. But you should do it together if you’re in a serious relationship.

Just a quick tip here, get your partner involved with money decisions before you say, “I do.” A lot of people don’t realize how their partner is with money, until years after getting married and starting a family. At that point, it’s too late.

Unfortunately, money problems are a big reason why couples get divorced. If one partner is spending loosely, racking up debt, and resistant to talking about money and financial goals, while the other is frantically trying to save every penny, there’s bound to be some tension.

Do yourself a favor and skip all the drama, download my free guide, “55 Smart Money Talks to Help Grow Your Money,” and start scheduling Money Dates. There’s some great stuff in there, including budgeting and bill tracker worksheets. I’ll put the link to download that workbook in the comments below.

But for this step, write down all your income. Don’t forget to include everything—full-time jobs, second jobs, freelance pay, babysitting money, and any other ongoing source of income.

If your income varies a lot like mine, base your budget on your average draw. My wife and I pay ourselves the same amount once a month, it doesn’t matter if it was a hugely successful month.

I’ve seen what happens to people that reach a certain level of financial comfort. They use the extra money to buy more stuff. And more stuff causes more problems. The more stuff people have, the more time, money, and effort it takes to maintain it all.

Step 2: Add up & categorize your monthly expenses

Think about your fixed monthly expenses such as your rent or mortgage, utilities, and transportation. Also list all your variable and discretionary expenses, including money that you use to pay your debts, eating out, subscriptions, having fun, and shopping.

Every dollar you spend should be accounted for. Make sure that you don’t forget any quarterly or annual expenses such as insurance premiums, homeowner’s association dues, the water and sewer bills, and property taxes.

In that “55 Smart Money Date Talks” workbook, you’ll also find worksheets in there to track your expenses each month and track recurring bills. This will help ensure you pay your bills on time, which makes you look like a superstar on your credit report.

Listing your expenses can be an eye-opening process. You might be surprised to find how much you spend eating out and having fun. And while this could be a stressor, it’s also an opportunity.

Every dollar that you spent over the past month that wasn’t necessary could potentially be recaptured and directed to one of your sinking funds, which I’ll cover in just a moment.

If you caught yourself saying, “I’d love to save money, but how do you find the money to save?” This is how.

Step 3: Subtract expenses from income

When you subtract your expenses from your income, you should be as near to zero as possible, but don’t get caught up in perfectionism. If there’s a big discrepancy, sure do some digging and find out where those dollars went. Otherwise, chalk up any missing dollars as miscellaneous spending.

If you find you have money left over, that’s called a “surplus.” If you spend more than you make (because you use credit cards), that’s called a “deficit.”

It can be very tempting to take the lazy approach in calculating your numbers, relying on a budgeting app or a spreadsheet. A decent spreadsheet can actually be very helpful, but I would recommend avoiding budgeting apps altogether at this stage.

Remember what I said earlier, “like words, numbers also tell a story?” Imagine learning how to read, which is what you’re doing with budgeting: you’re learning how to read numbers. Imagine that instead of actually picking up a book and reading it, that you took the lazy route and played the audiobook version.

Yes, you’re absorbing the knowledge in that book, but you’re not learning how to read which was the goal. Despite listening to the audiobook, reading the physical book would still be challenging.

The goal in creating a budget is to review your transactions and effectively share, in your own words, what the story behind those numbers mean. Why did you spend $100 on eating out this week? Was it because it was part of your budget, or was it because you were too busy or didn’t feel like cooking?

Clarity is the first step to building wealth.

I want you to schedule Money Dates with your partner every other week with the rule of no finger-pointing at who’s to blame. Go through your transactions together. Help each other and work as a team.

There’s a reason why I use cash for all my local transactions. I’m a spender, and using cash makes me hyper-aware about all of my purchases. I know I need to make that money last the entire month. Because of that, I have to be strategic about my purchases and occasionally I have to leave stuff behind at checkout.

Step 4: Pay yourself first using sinking funds

“Pay yourself first, and then spend the rest.” —Jim Dahle, MD

The life you want isn’t built with magic; it’s built with money. And you can’t hope to build an emergency fund, go on debt-free vacations, and invest for future opportunities if you wait until the end of the month.

Even if there’s a hundred bucks in the account, you’ll keep it in there out of fear. It’s our genetic programming trying to save us from the pain of bouncing a check and unknown money problems lurking in the shadows of our past.

A sinking fund is an account that’s completely separate from the account that you pay bills out of. It’s an account that’s specifically earmarked for a specific savings goal, such as your emergency fund. To fund this account, you should schedule an automatic transfer from your checking account, the day after you get paid.

Today, this is commonly referred to as, “paying yourself first.” And while a sinking fund isn’t budgeting, per se. It is the part of your budget that will make sure you have money to do the things that you say are important to you.

I prefer to use online banks for my sinking funds. Online banks typically have no minimums and no monthly fees. A few of them also allow you to open several accounts, with the ability to rename that account after your savings goal.

Here are some sinking funds that I’ve created for myself:

- Emergency fund —to make sure that I can survive a financial fallout.

- Vacation / Travel fund —because I love going on debt-free vacations. If I just put $5,000 on a credit card, it’s not going to be a relaxing trip for me. My thoughts are going to be fixated on all the work I’ll need to do to pay this trip off.

- 5-Year Goal fund —for larger purchases in life. People tend to buy a new car every 5-7 years, and having money for a down payment will keep your payments affordable.

- Grocery fund —because I love having 3-4 months’ worth of grocery money on hand. It’s financial security knowing that I can be out of work for a long time, and still put food on the table without having to rely on the government or debt.

- Kids activities fund —because, let’s face it, kids are friggin’ expensive between band and sports, and keeping them active throughout summer and winter breaks.

- Holiday fund —because the holidays aren’t a surprise. Neither should be your holiday spending. Take your holiday budget and break them up into monthly savings goals and put that money into a sinking fund so you don’t spend it.

- And my personal favorite, the Cash Cushion fund —because, we can’t plan for everything in life. This fund allows me to say “yes” to things that I don’t have a budget for, without feeling bad or getting my wife upset.

Try not to get discouraged if you can’t create all these sinking funds right away. It takes time and patience, but I’m confident that you can do it if you can get your partner on board.

Step 5: Track your spending

Once you’ve created your budget and automated savings to your sinking funds, monitor your cash flow. Again, that’s the money flowing in and out of your household. What you want to look out for is that you’re not saving in one area of your life, to the detriment of another.

Some people will find that their past will quickly catch up to them. You’ll want to pull a credit report to make sure there are no surprises. Make sure your partner does the same.

The Fair Credit Reporting Act (FCRA) requires each of the nationwide credit reporting agencies: Experian, Equifax, and TransUnion – to provide you with a free copy of your credit report once every twelve months.3

If a bill is out there in collections, waiting to cause havoc it will be in this report. The Federal Trade Commission (FTC) urges consumers to visit AnnualCreditReport.com.

The only place to get your free annual credit report, authorized by the FTC, is AnnualCreditReport.com. Websites that offer “free credit reports,” or “free credit scores,” or “free credit monitoring” are not part of the legally mandated free annual credit report program.

More information can be found at: https://www.consumer.ftc.gov/articles/0155-free-credit-reports

Conclusion

There you have it. I shared what a budget is and why it’s so hard to stick to them. It’s because students leave school without any financial skills. And while they end up pursuing their profession successfully, they later find themselves struggling financially.

Robert Kyosaki said it best, “A person can be highly educated, professionally successful, and still be financially illiterate.” If that’s you right now, it’s okay. Subscribe to my newsletter, where I share valuable tips that I don’t share anywhere on social media.

As one of my “Insiders,” you’ll also be invited to my private Facebook group, where you can share your wins and losses, ask questions, and join live sessions. I look forward to seeing you there!

Sources:

1) National Financial Capability Study, FINRA — https://www.usfinancialcapability.org/results.php?region=US#planning-ahead

2) Investment News, Financial literacy: An epic fail in America — https://www.investmentnews.com/financial-literacy-an-epic-fail-in-america-78385

3) Federal Trade Commission (FTC), Free Credit Reports —

https://www.consumer.ftc.gov/articles/0155-free-credit-reports