Last week, I noted the potential was high for a well-deserved break for stocks after a very strong start to the year. That seasonal weakness may have already begun. The S&P 500 is typically down in February, which joins September as the only other month to average a negative return. But as we shared last week, trouble usually brews in the later part of the month. In other words, don’t be overly worried should stocks see red in the coming weeks.

What we found last week was that similar to what we’ve been seeing, the consumer is resilient and, generally speaking, really just positive sentiments from CEOs. Many thought that things would be much worse now than they are but when they look around, they’re feeling fine. So that’s the theme for this week’s newsletter.

As we look forward, brace for a bumpy ride.

There were some unwelcome surprises in last week’s economic data that caused markets to reassess expectations for 2023. For example:

1. Inflation didn’t fall as fast as expected. Last week, the Consumer Price Index (CPI) showed inflation rose 6.4 percent, year-over-year, in January. That was an improvement over December’s pace and the seventh consecutive month of falling prices, but economists expected price increases to slow more quickly, reported Megan Cassella of Barron’s.

“Look into the details, and it is easy to see that the inflation problem is not fixed. America’s ‘core’ prices, which exclude volatile food and energy, grew at an annualized pace of 4.6% over the past three months, and have started gently accelerating. The main source of inflation is now the services sector, which is more exposed to labor costs…It is hard to see how underlying inflation can dissipate while labor markets stay so tight,” reported The Economist.

2. Consumer spending accelerated. Americans were in a buying mood. Retail sales, which is a proxy for consumer spending, rose 3.0 percent in January after declining in November and December of last year, reported the U.S. Census Bureau.

John Authers of Bloomberg opined:

“Another day, another item of evidence that the U.S. economy isn’t slowing down anything like as much as many had thought. U.S. retail sales in January rose the most in almost two years, reinforcing the narrative that consumer demand remains strong.”

Bullish sentiment in stock markets has been supported by the idea that inflation will continue to slow, and the Fed will be able to ease up on interest rates, reported Al Root of Barron’s. Last week, The Economist suggested stock markets may be overly optimistic. “Investors are pricing stocks for a Goldilocks economy in which companies’ profits grow healthily while the cost of capital falls…This is a rosy picture. Unfortunately, as we explain this week, it is probably misguided. The world’s battle with inflation is far from over.”

Note: The Goldilocks economy has been referenced numerous times since New Year’s, so let me explain. It’s a time where all economic conditions are just right. It’s not too hot nor too cold. Heat can cause inflation, and cold can create a recession.

Bond markets were less sanguine. After a chorus of Fed officials took the stage to let everyone listening know the federal funds rate would likely need to move higher – and stay higher – for longer, the bond market capitulated, reported William Watts of MarketWatch. As expectations shifted, the yield on a six-month Treasury moved above 5 percent for the first time since 2007 and the yield on a 10-year Treasury hit a new high for the year.

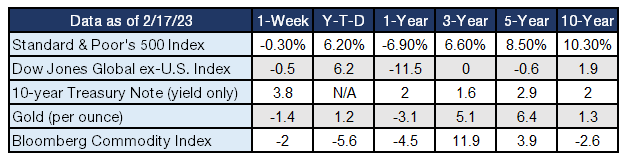

The Markets

Major U.S. stock indices finished the week mixed. The S&P 500 Index and Dow Jones Industrial Average moved lower, while the Nasdaq Composite Index finished slightly higher. Treasury yields rose across most maturities.

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance; MarketWatch; djindexes.com; U.S. Treasury; London Bullion Market Association.

Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

Macroeconomics

Most people thought that the economy would be in worse shape than it is but things, honestly, still seem fine. The consumer continues to spend and capital markets are beginning to look past inflation. It’s hard to believe that the Fed could tighten as aggressively as it has and not cause a recession, but there aren’t many signs of recession in the data that we’re looking at.

Let’s break this down…

We thought we’d be in worse shape by now, but things are still fine

“[OUR MIDDLE MARKET CLIENTS ARE] TRYING TO BE CAREFUL. THEY’RE TRYING TO MAKE SURE THEY CAN MAINTAIN MARGINS. THEY’RE TRYING TO MAKE SURE THAT THEY DON’T SEE A CHANGE IN FINAL DEMAND. BUT MOST OF THEM, HONESTLY WHEN YOU ASK THEM, THEY’RE SAYING, “I THOUGHT I’D BE IN WORSE CONDITION RIGHT NOW. I THOUGHT IT’D BE FACING MORE PRESSURE, AND THINGS ARE STILL FINE.” AND SO THAT’S A CONUNDRUM BECAUSE AT THE END OF THE DAY TRYING TO BE CAREFUL ON HIRING AND THINGS LIKE THAT IN THE GENERAL SENSE, YET THEY’RE SEEING THE FINAL DEMAND OF THEIR PRODUCTS AND SERVICE IS STRONG…SO I THINK OVERALL, MIDSIZED COMPANIES, I’M WITH A GROUP OF THEM LAST WEEK, AND THEY ALL KIND OF DON’T WANT TO SAY IT OUT LOUD, HONESTLY, THAT THEY’RE FINE, THEY’RE DOING FINE.”

-BANK OF AMERICA, CEO BRIAN MOYNIHAN

Consumers are resilient

“So let’s do consumer first. So — in the grand scheme of things, things haven’t changed particularly very much since earnings. Probably at the margin, things are slightly more positive…So broadly a continuation of the same themes. We can talk about the outlook a little bit, but in terms of what the data is showing us right now on the consumer side, it’s [positive].”

– JPMORGAN CHASE, CFO JEREMY BARNUM

“SO I THINK THE CONSUMER HAS BEEN MUCH MORE RESILIENT THAN PEOPLE EXPECTED. I THINK THERE HAVE BEEN BEHAVIOR PATTERNS BASED ON THE WAY PEOPLE LIVE AND WORK. THEY’VE AFFECTED PEOPLE’S DISPOSABLE INCOME AND HAVE SHIFTED THE WAY THEY’RE DOING CERTAIN THINGS, AND THERE’S BEEN A LONG RUN OUT ON THAT.”

– GOLDMAN SACHS, CEO DAVID SOLOMON

Inflation is still high

“The all items index increased 6.4% for the 12 months ending January; this was the smallest 12- month increase since the period ending October 2021…The index for shelter was by far the largest contributor to the monthly all items increase, accounting for nearly half of the monthly all items increase, with the indexes for food, gasoline, and natural gas also contributing” – US Bureau of Labor Statistics

“There’s no doubt that inflation is impacting consumer decisions, and it’s looking likely that inflation will continue into next year, albeit at a moderating pace” – BJ’s Wholesale Club, CEO Robert Eddy

Can the Fed really be this aggressive and not cause a recession?

“And so [our economists are] sitting and saying, I know it’s got to come. The Fed can’t tighten this aggressively and not cause [a recession] — and I understand that, but they don’t see it. And that’s why I keep saying that they’ll just move out a little bit and get a little less severe each time our team comes out.” – Bank of America, CEO Brian Moynihan

A strong consumer is ultimately a good thing

“…and that’s a conundrum for the Fed to slow it down. And it’s a good thing. The best thing about the U.S. is a consumption-led economy by U.S. consumers who spend money very well, is a nice place to be. And that’s the tension that’s going on.” – Bank of America, CEO Brian Moynihan

What do you value most?

The 2022 Modern Wealth Survey, which is conducted for Charles Schwab by Logica Research, asked Americans whether personal values are more important to life decisions than they once were. The majority said yes.

“Almost three-quarters of Americans (73%) say their personal values guide how they make life decisions more today than they did two years ago, and nearly an equal number (69%) say that supporting causes they care most about are a top consideration when it comes to their financial decisions…When asked which personal values are their biggest motivators, Americans prioritize doing what’s best for others, including the environment and the greater good as well as their family and friends, followed by saving more and reducing unnecessary spending.”

Defining and prioritizing values takes time and can be a challenging exercise. The Good Project, a research initiative at the Harvard Graduate School of Education’s Project Zero, offers an online value sorting activity. Visitors review a list of 30 values and choose 10 to begin. The list includes options like:

- Fame and success,

- Courage and risk taking,

- Creativity and originality,

- Power and influence,

- Hard work and commitment,

- Faith,

- Pursuing the common good,

- Recognition in your field, and

- Solitude and contemplation.

A majority of each generational group that participated in the Modern Wealth Survey agreed that values affect their investment choices: 68 percent of Baby Boomers, 73 percent of Gen X, 75 percent of Millennials, and 82 percent of Gen Z.

Overall, “When looking at the factors that influence investing decisions, a company’s reputation (91%) and its corporate values (81%) are almost as important as more traditional factors like a company’s performance (96%) and its stock price (93%). As personal beliefs and interests become more important, many investors (84%) are also interested in having a more personalized investment portfolio.”

When you think about money and investing, what is important to you? It’s probably something we should talk about.

Weekly Focus – The only currency that matters

“At the end of your life, you will never regret not having passed one more test, not winning one more verdict or not closing one more deal. You will regret time not spent with a husband, a friend, a child, or a parent.

—Former First Lady, Barbara Bush

As we close out Week 8, I want you to imagine that you are financially secure, that you have enough money to take care of your needs, now and in the future. My question to you is…

How would you live your life? What would you do with the money? Would you change anything? Let yourself go. Don’t hold back your dreams. Describe a life that is complete, that is richly yours.

If you would like to collaborate on this project, email me your response. I’ll let you know if you’re on the right track.

For example, someone who wants to spend more time with their grandkids in retirement may be able to find ways to spend more time with grandkids even before retirement. With is level of awareness, your financial advisor now has the flexibility in offering different and potentially unconventional options that still address your true goal (e.g., perhaps you can put off retirement and focus on finding ways to start spending more time with your grandchildren).

I wrote this week’s Focus in the hopes of liberating you from the self-defeating belief that you have to work yourself into the ground, worry about money your entire life, and enter retirement full of fear about the future.

As you work to complete the above exercise, I encourage you to say or describe anything; nothing is off limits, everything and anything is possible.

I am here to help you find ways to savor the only currency that truly matters: time.

Stay wealthy,

Tom Martin, WMCP

Wealth Advisor, Vaylark Financial Services

“Wealth Designed. Life Defined.” – that’s my motto.

P.S. Please feel free to forward this commentary to family, friends or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.