Donald and Sarah

Status: Preparing for retirement in 2-3 years

The Big Question

Donald and Sarah came to us because they had a big question - Do we have enough to retire? Despite their modest income, Donald had saved a million dollars in his 401(k) at work. He's been maxing out his 401(k) plans, they're both debt-free including the mortgage, but they didn't have other investments.

The problem was that they didn't have an idea where they stood. The markets were tanking, and they saw their 401(k) drop from a $1,000,000 to $850,000 (-15%). In addition, inflation is at an all-time high of 8.5%, the Fed is hiking interest rates 0.50% at a clip, and the Tax Cuts and Jobs Act sunsetting would mean higher taxes in retirement.

The Plan

Donald and Sarah were rightfully scared when we started out. They lost a lot of money in Donald's 401(k) within the spread of a couple of months, and they were afraid.

What they didn't realize was that the 401(K) is a passive, wealth accumulation vehicle. While they're exceptional at growing account balances, they're not so effective at mitigating loss outside of fund selection or moving to cash.

We started by having a conversation on what their ideal retirement would look like, understanding that there are different phases to retirement. First, we start out in the 'go-go phase," where the would be more active and spend time traveling and Donald could enjoy his favorite past-time: golfing.

Also, while Donald and Sarah were focused on the term "retirement," Donald didn't want to stop working entirely. He thought it would be enjoying to take a part time job at his golf club. While it wouldn't be a comparable transition from his current job, it was most certainly less stressful and connected to something he loved. From there, we worked to help them consolidate old 401(k)s into IRAs, which help him implement some investment strategies to defend his portfolio from substantial loss.

We also set up a Roth conversion strategy would would allow them to reduce thousands and thousands of dollars in avoidable taxes once the TCJA sunsets. We made sure they had the right insurance policies in place to protect them and even reviewed their living wills, to ensure everything looked smooth. They understood the value in taking care of these things before they got old and had less cognitive ability.

Finally, we put together a customized investment strategy that would generate all he income they needed for the rest of their lives to live comfortably.

The Result

By organizing their and simplifying their finances, we gained clarity and control over their situation. Through our retirement planning conversations, we discovered a viable path for Donald to retire, and doing the things that reduced his stress and increased his wellness.

Since Donald wasn't quitting work altogether, and instead opted to work part time doing something enjoyable, he was still able to bring some income into the home, while delaying claiming Social Security early, which we discovered wouldn't be much of a benefit at this time.

More than that, Donald and Sarah are enjoying true peace of mind in knowing that their retirement portfolio isn't collapsing just before retirement. The money would be there and income ready to be turned on whenever they wanted to push the button.

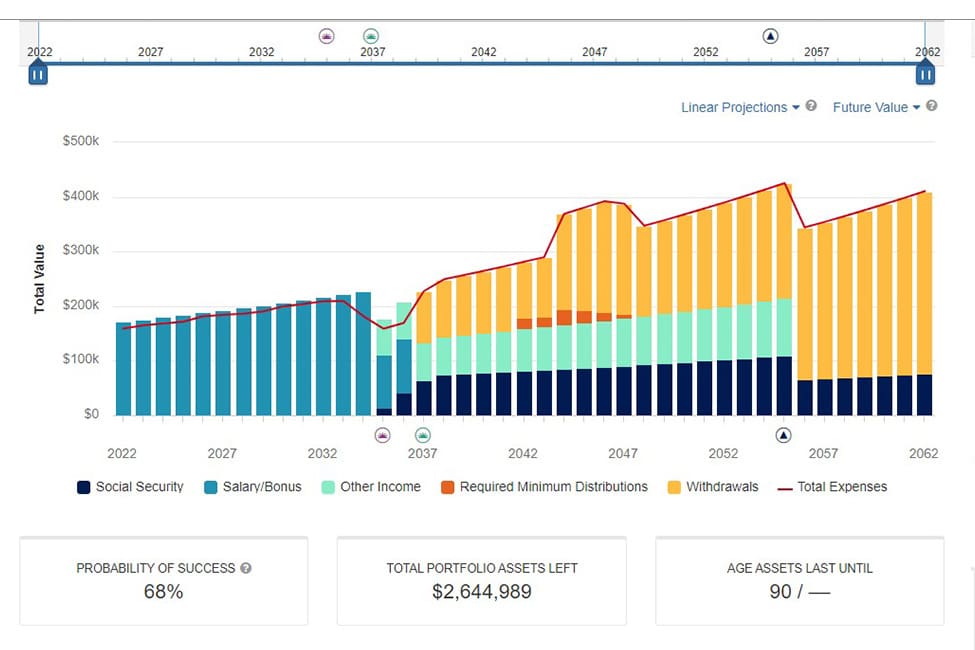

This is a real cash flow illustration for “Donald and Sarah.”